With a market cap of $99.5 billion, Adobe Inc. (ADBE) provides creative, marketing, and document management solutions through its Digital Media, Digital Experience, and Publishing and Advertising segments. It serves individuals, businesses, and enterprises worldwide with products and services for content creation, customer experience management, e-learning, advertising, and AI-powered applications.

Shares of the San Jose, California-based company have lagged behind the broader market over the past 52 weeks. ADBE stock has declined 38.9% over this time frame, while the broader S&P 500 Index ($SPX) has risen 26.3%. Moreover, shares of the company have decreased 30.9% on a YTD basis, compared to SPX's 7.9% gain.

Looking closer, the creative software giant stock has underperformed the State Street Technology Select Sector SPDR ETF's (XLK) 54.9% surge over the past 52 weeks.

Shares of Adobe tumbled 7.6% following its Q1 2026 report on Mar. 12 mainly due to the surprise announcement that CEO will step down once a successor is named, creating leadership uncertainty during a critical AI transition phase. Investor concerns were amplified by ongoing skepticism about Adobe’s ability to monetize its AI investments, especially as new AI-driven competitors threaten its traditional subscription model.

Despite this, Adobe reported better-than-expected Q1 revenue of $6.40 billion, adjusted EPS of $6.06, and Creative subscription revenue of $4.39 billion, along with Q2 guidance of $6.43 billion - $6.48 billion, roughly in line with forecasts.

For the fiscal year ending in November 2026, analysts expect Adobe's EPS to grow 11.3% year-over-year to $19.14. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

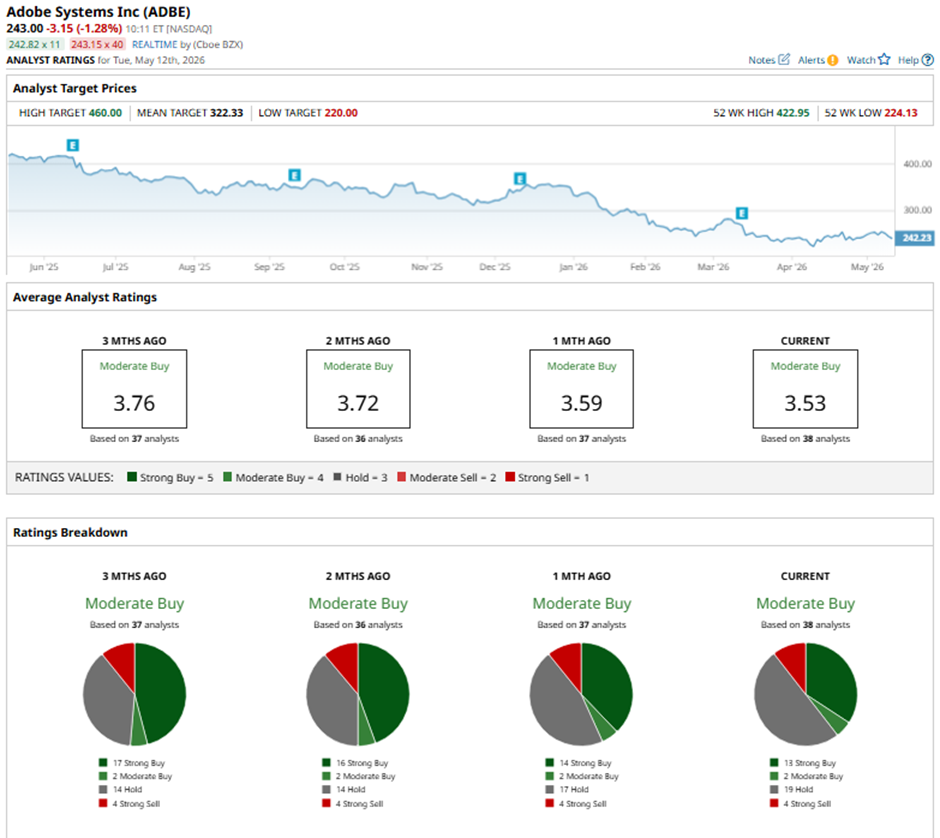

Among the 38 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, two “Moderate Buys,” 19 “Holds,” and four “Strong Sells.”

On Apr. 17, RBC Capital lowered its price target for Adobe to $350 while maintaining an “Outperform” rating.

The mean price target of $322.33 represents a 32.6% premium to ADBE’s current price levels. The Street-high price target of $460 suggests a 89.3% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Quantum Computing Takes Off After Earnings, Here's What Barchart Data Says Comes Next for QUBT Stock

- BuzzFeed Skyrockets on Byron Allen Takeover. What Comes Next for BZFD Stock.

- Earnings Sent Fastly Stock Down Bad, but Don’t Miss the Bigger Picture with FSLY Shares Up 85% YTD

- 2 Market-Beating Tech Stocks That Could Become Even Bigger Winners in AI