For years, Nvidia (NVDA) has been the poster child of premium growth, consistently commanding a valuation far above the broader market as investors bet heavily on its dominant position in artificial intelligence (AI). From powering data centers to enabling the explosive rise of generative AI following ChatGPT, Nvidia has delivered the kind of earnings growth that typically justifies elevated multiples. But now, something unusual is happening—and it has caught Wall Street’s attention.

For the first time in over a decade, Nvidia is trading at parity with the S&P 500 ($SPX) based on its forward price-to-earnings (P/E) ratio. In other words, the market is no longer assigning a premium to the most valuable company in the world. At the same time, analysts continue to raise earnings forecasts, with demand for AI chips showing little sign of slowing, and Nvidia is still expected to contribute a significant portion of the S&P 500’s overall earnings growth in the coming years.

For investors, this raises a critical question: Is the market finally right to normalize Nvidia’s valuation, or is this a rare opportunity to buy a high-quality growth stock at a discount? Let’s take a closer look!

About Nvidia Stock

Nvidia Corporation is a premier technology firm known for its expertise in graphics processing units and artificial intelligence solutions. The company is renowned for its pioneering contributions to gaming, data centers, and AI-driven applications. NVDA’s technological solutions are developed around a platform strategy that combines hardware, systems, software, algorithms, and services to provide distinctive value. The chipmaker’s market cap stands at $4.24 trillion, ranking it as the most valuable company in the world.

Shares of the AI darling have dropped 5% on a year-to-date (YTD) basis. NVDA stock came under pressure amid a broader market rotation tied to the war in Iran and concerns about the sustainability of AI spending.

Nvidia’s Valuation Slips to S&P 500 Parity. What Does It Signal for NVDA Stock?

As fears over the economic fallout from the war in the Middle East unsettled global equity markets last month, Nvidia’s forward price-to-earnings (P/E) multiple fell to its lowest level since before ChatGPT ignited the AI boom. Investors use the forward P/E multiple to assess stock valuations based on their expected future earnings. The multiple is calculated by dividing a company’s current share price by its projected earnings per share (EPS) over the next 12 months. And the sharp decline in Nvidia’s forward P/E has ignited debate among investors over whether it’s time to buy the dip, with some bargain hunters already beginning to swoop in.

Even more striking, the selloff in Nvidia shares compressed the chipmaker’s forward P/E multiple to a level that aligned with the average for the S&P 500 index. A Goldman Sachs trading desk note circulated on Monday stated that Nvidia’s forward P/E ratio has fallen to match the broader S&P 500 for the first time in over a decade. NVDA stock has even traded at a discount to the S&P 500 several times since the start of the Iran war. That ended a 13-year streak of trading at a premium to the benchmark index since February 2013, according to Dow Jones Market Data.

Things begin to seem irrational, even paradoxical, when you consider that Nvidia’s earnings are expected to grow at a much faster rate than overall S&P 500 earnings. Analysts expect aggregate S&P 500 earnings to rise 19% in 2026, compared with an average growth forecast of more than 70% for Nvidia in its current fiscal year. This is noteworthy because investors typically assign higher P/E multiples to fast-growing companies than to those with slower earnings growth. Notably, Nvidia has often traded at a premium of more than 10 points above the S&P 500. Goldman analysts pointed to another striking disconnect: Nvidia alone is projected to account for roughly 21% of the S&P 500’s total earnings growth in 2026. In essence, investors are no longer willing to pay a premium for Nvidia’s growth.

Moreover, analysts have largely been raising their forecasts for Nvidia’s future earnings growth. Over the past three months, the company has seen 43 upward revisions and just two downward revisions to its fiscal 2027 earnings estimates. Of course, we can also view NVDA’s valuation “paradox” through the lens of higher Treasury yields, which have pressured valuations for Nvidia and its Magnificent Seven peers even as earnings expectations have improved. Even so, such a low valuation looks entirely unjustified.

The valuation parity with the S&P 500, combined with Nvidia hitting a strong support zone near the $170 level earlier this week, leads me to believe this area could serve as a solid floor for the stock. We even saw early confirmation on Tuesday, when NVDA shares staged a relief rally from that zone amid hopes that an end to the Middle East conflict may be in sight. And even after that rally, NVDA’s forward P/E multiple stands at 21.03x, roughly in line with the S&P 500’s current valuation of 20.5x.

Meanwhile, NVDA investors have one more reason for optimism if history is any guide. The stock fell 6.5% in the first quarter, marking its second consecutive quarterly decline, its longest losing streak since a three-quarter slide that ended in late 2022. Over the past decade, Nvidia has posted an average gain of about 12% in the month following a losing streak of two or more months, according to Dow Jones Market Data.

Should You Snag the Dip in NVDA Stock Now?

Putting it all together, I believe now may be an opportune time to buy NVDA stock, as we’re seeing a rare alignment of multiple confluence factors—both technical and fundamental. Let me explain in more detail. First, analysts are increasing their earnings forecasts for NVDA as demand for AI chips remains robust and is expected to stay strong for years to come. Second, the stock hit a strong support zone from which it has bounced multiple times in the past. Third, NVDA stock looks stupidly cheap, providing a huge margin of safety. Finally, the chipmaker’s track record suggests there is potential for a rebound in the months ahead.

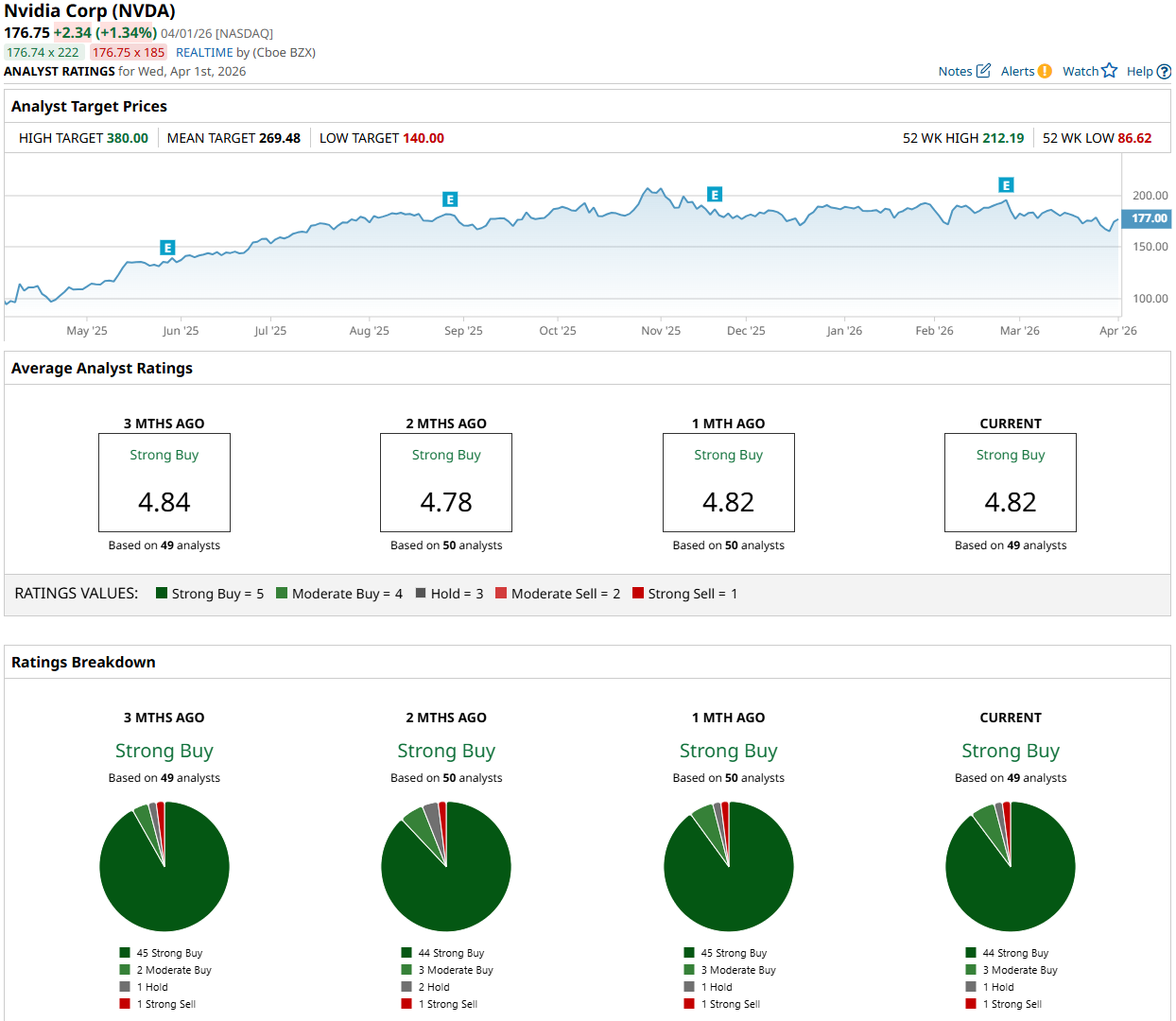

Wall Street analysts remain highly bullish on NVDA, as reflected in the stock’s “Strong Buy” consensus rating. Among the 49 analysts covering the stock, 44 have a “Strong Buy” rating, three assign a “Moderate Buy” rating, one recommends holding, and one issues a “Strong Sell” rating. Notably, most analysts have maintained their ratings over the past three months. The average price target for NVDA stock is $269.48, implying 52.5% upside from current levels.

On the date of publication, Oleksandr Pylypenko had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Has Been Steady Amid the Iran War: Is It Still a Buy?

- Boeing Jumps on New Pentagon Deal. Should You Buy BA Stock Here?

- This Tech Stock May Be About to Short Circuit Near 52-Week Highs

- A Giant Meatpacking Strike Isn’t Enough to Dent the Bull Case for JBS Stock, According to Bank of America