Apple (AAPL) has received its fair share of criticism in the past when it comes to the iPhone. From slow development cycles to reduced demand, the market has punished the stock without hesitation. Yet every time the iPhone maker looks to have plateaued, it strikes back. The recent note from Morgan Stanley analyst Erik Woodring shows how bullish the firm is on AAPL stock. And it has the numbers to back its bullish thesis.

The investment firm’s late 2025 AlphaWise Smartphone Survey shows upgrade rates in China going up by nine points YoY. Global blended iPhone upgrades have never been as high as they are now, while the switching rate to Apple has also reached a five-year high. On top of all this, 27% of the survey participants have shown an interest in the foldable iPhone. Bank of America Securities has already predicted 20 million sales of the foldable iPhone, with the launch just around the corner. Morgan Stanley now forecasts 6% iPhone revenue growth in FY26, compared to the Wall Street consensus of 3%.

About Apple Stock

Apple designs and manufactures devices and accessories such as the iPhone, iPad, Mac personal computers, tablets, home devices, and wearables. It also provides various services like AppleCare and the App Store. The company is headquartered in Cupertino, California.

AAPL stock has roughly mirrored the broader market’s performance over the last 12 months. During this period, it has given returns of 13.35% compared to the S&P 500 Index’s ($SPX) 16% returns. If analyst sentiment is anything to go by, the stock could significantly outperform the market over the next 12 months.

Apple is trading at a forward P/E of 29.12x, pretty close to its five-year average of 28.7x. When one considers this valuation in the context of Morgan Stanley’s report, it appears the market is yet to price that iPhone growth in. Morgan Stanley believes the foldable iPhone will be a hit and boost FY27 iPhone revenues. Its estimates are 4% above consensus, which is an extremely bullish position and deserves a valuation premium.

The above estimates are not baked into the relatively disappointing 9.5% consensus earnings growth in FY27. Once analysts start including improved iPhone growth numbers, this earnings growth number can significantly improve. Wall Street expects the firm to grow its earnings by 11.21% in 2028 and 20.09% in 2029. The earnings landscape could significantly change if the foldable iPhone is a hit.

Apple's Q1 Earnings

Apple reported its Q1 2026 earnings on Jan. 29. The net income of $42.1 billion was a significant improvement on the $36.33 billion during the same period last year. Sales in China, Taiwan, and Hong Kong went up by 38% during the quarter. iPhone revenue was $85.27 billion compared to expectations of $78.65 billion, while the Services segment revenue of $30.01 billion fell just below the consensus of $30.07 billion. Gross margins improved slightly from 47.5% last year to 48.2% this quarter.

CEO Tim Cook called the iPhone demand staggering. The number of people upgrading their phones in mainland China reached an all-time high. While the demand is expected to stay strong, management pointed out that memory price inflation and advanced node availability have resulted in conservative guidance. Having said that, gross margins are expected to stay within 48% and 49% in the ongoing quarter.

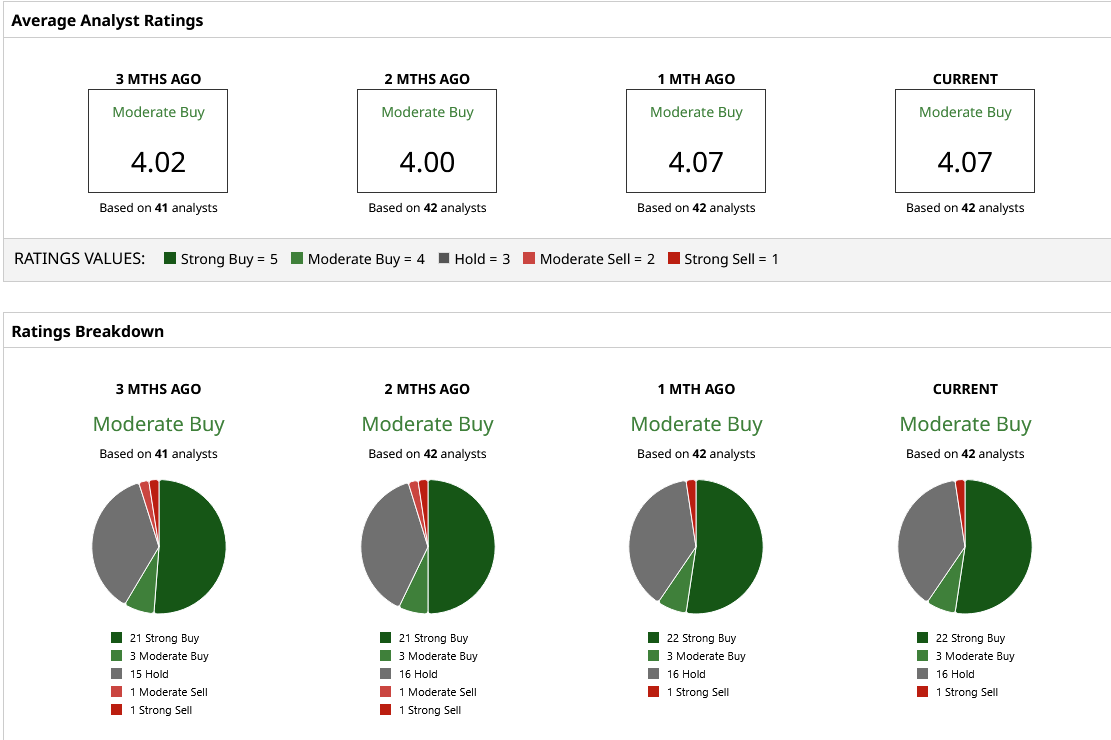

What Are Analysts Saying About AAPL Stock?

AAPL stock has a mean target price of $295.90 on Wall Street, which suggests 17.5% upside from here on.

Apart from Morgan Stanley, other research firms have also reiterated their bullish stances on the stock. On March 23, Bank of America Securities reiterated its “Buy” rating, though it also adjusted the price target from $325 to $320. Earlier in the month, analysts from Citi, Bernstein, Goldman Sachs, Evercore ISI, and Wedbush Securities also reiterated their bullish stances. Wedbush Securities’ Daniel Ives currently has the highest price target of $350 on the stock, which reflects almost 40% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Berkshire Hathaway Is Betting Big on Little-Known Tokio Marine. Should You Buy the Stock Here?

- The Gold Paradox: Why Investors Aren’t Finding Safety in Precious Metals During a Global Crisis

- Flutter Stock Could Be a Big Winner as Lawmakers Zero In on Prediction Markets. Should You Buy FLUT Here?

- United Airlines Stock Is Rebounding as Oil Prices Fluctuate. Should You Buy the UAL Stock Dip?