Geopolitical tremors are shaking global markets again. As U.S.-Iran strains push oil prices higher, travel demand is turning cautious, and airline stocks are slipping. But this time, it is not just fuel costs rattling the sector, but growing ground-level disruptions are adding a new layer of uncertainty.

On Feb. 14, a partial government shutdown began as it left thousands of Transportation Security Administration (TSA) agents unpaid, triggering rising absenteeism and operational strain. U.S. Transportation Secretary Sean Duffy has warned that prolonged staff shortages could lead to airport disruptions, even closures in smaller hubs. Acting TSA head Adam Stahl echoed the concern, suggesting the system is already stretched thin. The implications are longer security lines, potential travel chaos, and a dent in peak seasonal demand. Naturally, investors are uneasy, with airline stocks facing renewed pressure.

Yet even as pressures build both in the skies and on the ground, Delta Air Lines (DAL) stands out as a relatively steady player. However, Delta may be better positioned to handle the double hit. Its premium-heavy customer base and strong corporate travel demand provide a cushion against potential volume softness. At the same time, the airline has already absorbed a roughly $400 million fuel cost hit and still expects earnings to remain on track, highlighting solid pricing power and operational discipline. Its Trainer Refinery helps offset a meaningful portion of fuel cost volatility, and industry-leading margins offer added protection when conditions turn rough.

And importantly, with the stock already down about 15% from its recent highs, a fair share of the negative sentiment appears to be baked in, making the current setup a bit more balanced than it may seem at first glance. So, while the aviation sector faces both airborne and ground-level disruptions, does Delta have enough lift to rise above the turbulence, or are more headwinds waiting ahead?

About Delta Air Lines Stock

Delta Air Lines has been around since 1924, and over the years, it’s grown into one of the world’s leading carriers, connecting people across more than 300 destinations globally. Headquartered in Atlanta, Delta runs a massive network through key U.S. hubs and major international gateways, backed by a fleet of over 1,300 aircraft.

But beyond the scale, what really defines Delta is its focus on experience. With around 100,000 employees powering up to 5,500 daily flights, the airline leans heavily into service, innovation, and reliability. Having flown over 200 million passengers in 2025, Delta continues to position itself as a premium, customer-first airline in an increasingly competitive sky. Its market capitalization currently stands at around $41.4 billion.

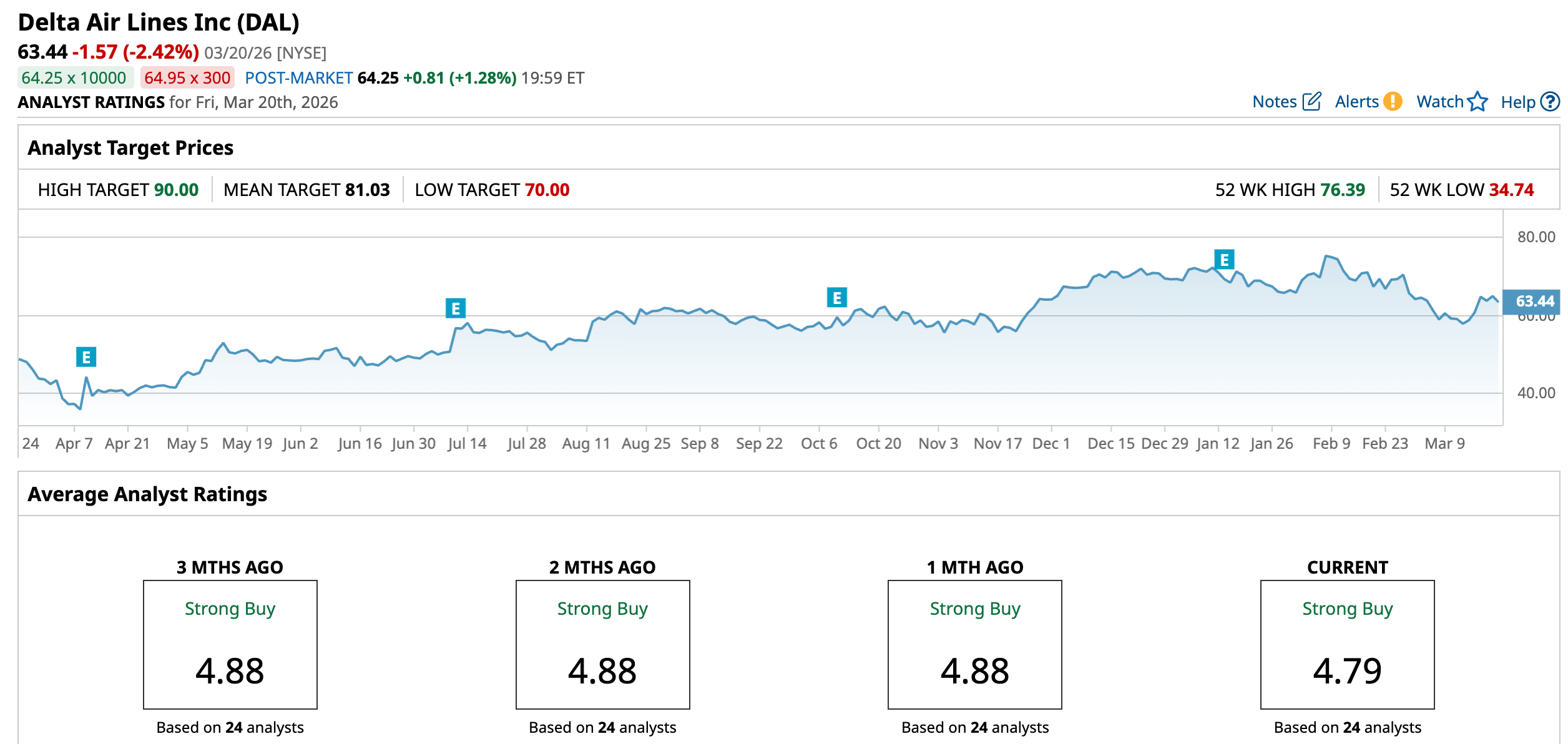

DAL’s stock chart reflects a blend of strong momentum, a pause, and now early signs of a rebound. Backed by solid earnings and robust corporate travel demand, DAL climbed to an all-time high of $76.39 in February, capping a strong run. Even after some pullback, the stock remains up 35.12% over the past 52 weeks and 6.16% over the last six months, pointing to underlying strength.

Yet in the near term, the tone softened. Over the past three months, DAL has declined about 10.72%, with a 8.64% drop over the past month, as concerns around rising fuel costs and travel demand weighed on sentiment. But momentum appears to be shifting again. In the last five days alone, the stock has rebounded 7.93%, suggesting renewed buying interest. This recent rally has been fueled by the company’s upbeat financial update.

Technically, this bounce is starting to make sense. Volume patterns are turning positive, with increasing green bars indicating stronger participation from buyers. The 14-day RSI, which had dipped close to oversold levels earlier in March, has now recovered to 47.76, moving back into neutral territory with a slight bullish tilt.

At the same time, the MACD oscillator signals improving momentum. The MACD line has recently crossed above the signal line, and the histogram has turned positive. Both are classic signs that bullish momentum may be building. While not fully out of the woods, DAL’s chart is beginning to hint at a potential recovery taking shape.

Valuation-wise, Delta Air Lines is not exactly screaming “expensive” right now. Priced at around 9.62 times forward adjusted earnings, it is cheaper than most of its airline peers. Even its price-to-sales ratio of 0.59 times sits below both the industry average and its own historical levels.

Delta Air Lines’ Q4 Earnings Snapshot

Delta Air Lines dropped its Q4 numbers on Jan. 13, pulling in a record $14.6 billion in adjusted revenue, although that inched up by just 1.2% year-over-year (YOY) and slightly beat expectations. Domestic travel showed some softness, largely tied to disruptions like the government shutdown. But Delta managed to offset that with solid momentum elsewhere such as international routes, premium cabins, loyalty programs, and corporate travel, which all stepped up and formed the backbone of its growth story heading into 2026.

What’s driving this resilience is Delta’s focus on a more premium, higher-income customer base. These travelers are less sensitive to economic bumps, and they are spending more – not just on tickets, but across the broader Delta ecosystem. A big piece of that comes from its partnership with American Express (AXP). In 2025 alone, remuneration from Amex cards jumped 11% YOY to $8.2 billion, as affluent customers continued to swipe Delta co-branded cards and double down on loyalty rewards.

International travel, too, remains a strong pillar. Delta’s overseas business grew 5% annually in Q4, powered by demand across Transatlantic and Pacific routes. Moreover, about 90% of its corporate clients expect travel demand to either rise or hold steady in 2026, signaling that business travel still has legs.

Margins, though, told a slightly mixed tale. Higher costs and softer fares put some pressure on profitability. Adjusted EPS slipped 16% YOY to $1.55, but aligned with Delta’s own guidance and Wall Street’s projections. These proved steady enough to keep investor confidence intact.

Even as macro clouds gather, Delta Air Lines is telling a story of resilience rather than retreat. CEO Ed Bastian recently pointed out that most of Delta’s revenue flows from premium offerings, giving it a cushion that most budget carriers simply don’t have when costs start rising.

In fiscal 2025, Delta generated a record $4.6 billion in free cash flow, delivered a 12% return on invested capital, and maintained double-digit margins, all while strengthening what management calls its most solid balance sheet yet. Strong operating and FCF allowed the airline to chip away at debt, bringing its leverage ratio down to 2.4x, well within reach of 2026 targets.

What’s more telling is the near-term momentum. At the J.P. Morgan (JPM) Industrials Conference, Delta signaled stronger-than-expected demand, nudging its Q1 2026 revenue outlook higher to around $15 billion to $15.3 billion range, ahead of earlier projections. Even with fuel costs rising and weather disruptions in play, EPS is still expected to land between $0.50 and $0.90. The company is all set to hold a live conference call and webcast to discuss its March quarter financial results on Wednesday, April 8.

Looking further ahead, management anticipates fiscal 2026 EPS between $6.50 and $7.50, suggesting that, despite the noise, demand remains intact and the airline is firmly in control of its flight path.

Meanwhile, analysts monitoring Delta predict the airline company’s EPS for fiscal 2026 growing 17.7% YOY to $6.85, and then rising by another 17.37% annually to $8.04 in fiscal 2027.

What Do Analysts Expect for Delta Air Lines Stock?

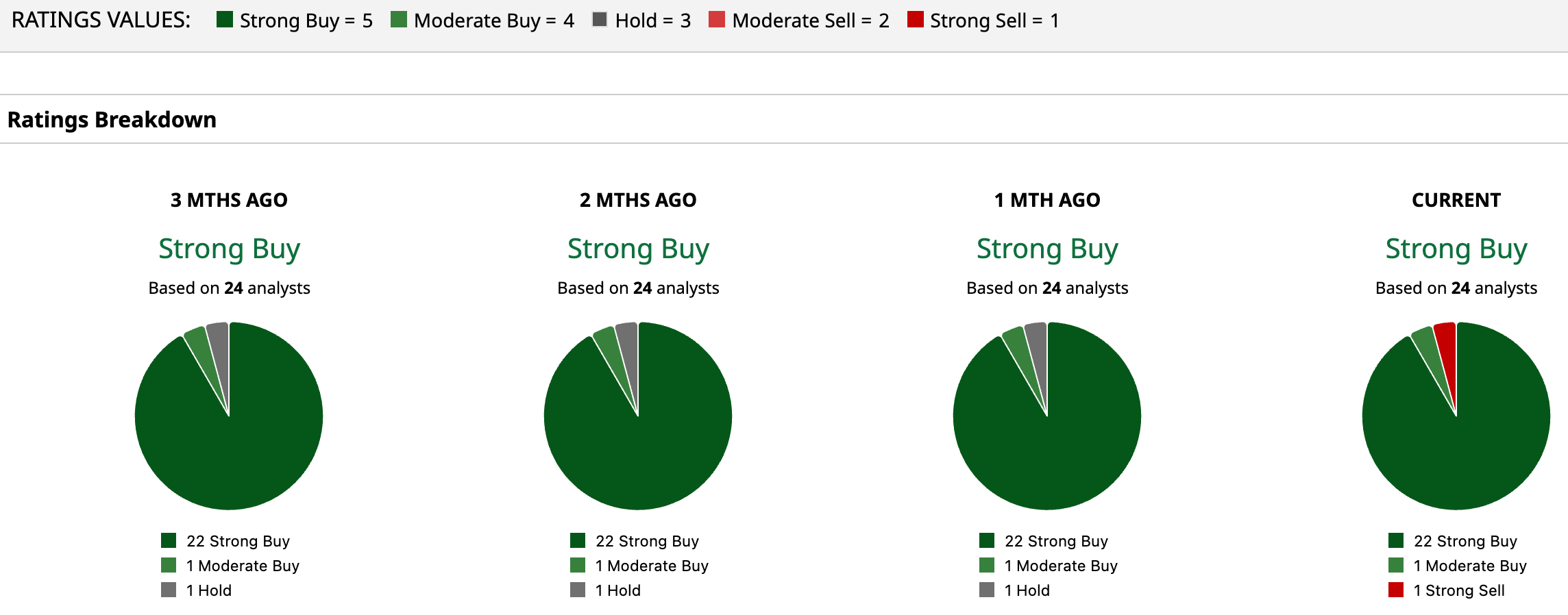

Wall Street, for now, is firmly in Delta’s corner. DAL stock carries a “Strong Buy” consensus overall, with 22 of the total of 24 analysts recommending a “Strong Buy,” one leaning moderately bullish and advising a “Moderate Buy,” while the remaining one is outright skeptical, giving a “Strong Sell” rating.

As for where the stock could head next, the mean price target of $81.03 suggest that DAL has potential upside of 27.7% from the current levels. The Street-high of $90 implies the airline stock could rise as much as 41.9% from here.

Final Thoughts on DAL Stock

Right now, Delta Air Lines is sitting in a bit of a mixed zone. Short-term risks like airport disruptions, softer travel demand, and rising fuel costs are very real and could keep the stock under pressure. But if we zoom out, Delta’s premium-focused model, solid execution, and confident management outlook suggest it’s built to handle these bumps better than most.

The valuation also looks fairly reasonable after the recent dip, which balances the risk side a bit. And while investors wait for things to stabilize, there’s a small perk – Delta is paying dividends. So sure, the ride may stay choppy for now, but for patient investors, the overall setup doesn’t look too bad.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart