Oracle (ORCL) has been under pressure recently, and that’s why the latest analyst call is important. Analyst Siti Panigrahi at Mizuho wrote that “bearish concerns” surrounding Oracle are easing after the Q3 report while maintaining an “Outperform” rating on the shares but cutting the price target to $320 from $400 due to peer multiple contraction rather than a change in their underlying thesis.

The old thesis was rather straightforward: Oracle’s aspirations in AI were legitimate, but the company would need to go heavily leveraged to support that investment in the data center business. The new argument is that a significant part of that business growth can be supported through customer prepayments and bring-your-own-hardware models.

About Oracle Stock

Oracle is one of the largest enterprise software and cloud infrastructure companies in the world, is based out of Austin, Texas, and has a market capitalization of approximately $444.9 billion. Oracle has become increasingly prominent in terms of its position within the overall AI infrastructure landscape as Oracle Cloud Infrastructure grows rapidly and wins larger deals within the AI space.

ORCL's stock price has also seen significant volatility. The stock is currently at about $155, which is near the lower end of its 52-week range of $118.86 to $345.72. This means that the stock is up about 31% from the low end of its 52-week range but still down about 55% from the high end of its range.

Regarding the valuation, the stock is no longer cheap but also no longer overpriced from the perspective of the old-school value investor. The stock is at 25.72 forward earnings and 7.75 sales. When the company is growing total revenue at more than 20% and cloud infrastructure at more than 80%, the stock price no longer seems overpriced from the perspective of the old-school value investor.

The stock also offers a quarterly dividend of $0.50 per share. The next dividend is payable on April 24, 2026, to the shareholders of record as of April 9, 2026.

Oracle Beat on Earnings—And the Backlog Was the Real Story

Oracle reported its Q3 2026 earnings, which were undoubtedly impressive. Revenue was up 22% year-over-year (YoY) to $17.2 billion, EPS was up 21% YoY to $1.79 on a non-GAAP basis, and cloud revenue was up 44% YoY to $8.9 billion.

But the real story was the company’s cloud infrastructure revenue, which was up 84% YoY to $4.9 billion—which suggests that the company’s AI push is actually paying off in terms of revenue growth and not just hype.

The real shocker, though, was the remaining performance obligations. Oracle reported RPO of $553 billion at the end of the quarter, up 325% YoY and rising by $29 billion sequentially. It is massive, and the management deserves much more credibility when they talk about the acceleration of revenue over the next few years. Oracle also reiterated its revenue guidance of $67 billion for FY2026 and increased its revenue guidance to $90 billion for FY2027. For Q4 FY26, the management guided revenue growth of 19% to 21% and non-GAAP EPS of $1.96 to $2.00.

Another detail I liked was that the company said that much of the RPO growth in recent times was driven by large AI contracts, as the necessary equipment is either funded upfront by the customer prepaying the contracts or the customers provide the necessary equipment themselves. In simpler words, the company may not have to stretch itself as much as the market thinks it has to, at least not as much as the market thinks it has to.

Another highlight was that the improvement in the ability of AI code generation has helped improve the efficiency of the company’s internal software development, allowing them to create more SaaS applications at lower costs.

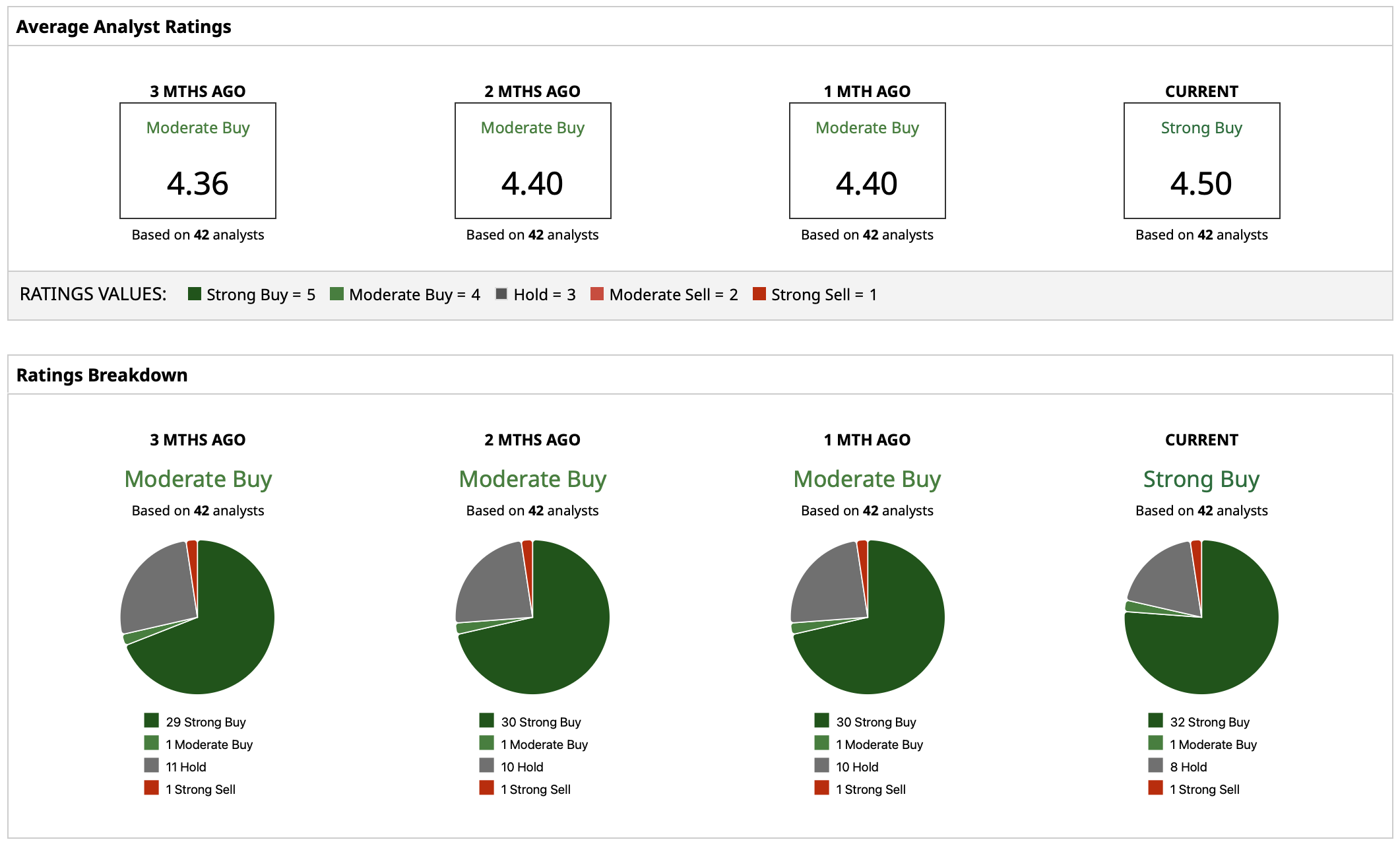

What Do Analysts Expect for ORCL Stock?

The analyst consensus is still favorable, with a “Strong Buy” rating consensus, and a high target is $400, the mean target is $257.54, and the low target is $155.00. The mean target of $257.54 represents a 65% upside from the current share price of $155.79.

What this tells us is that the market still sees ORCL as a bit of a controversial stock, as some analysts think the company is worth much more given the AI contracts, while others think that the current stock price is much more appropriate, as evidenced by the low target of $155, which is almost exactly the current stock price.

The $320 target that Mizuho has, even after the target was cut, represents an upside of 105%, which is pretty remarkable for a company of this size.

On the date of publication, Yiannis Zourmpanos had a position in: ORCL . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart