Apple (AAPL) has long dominated the premium end of the personal computing market, but its latest launch could signal a strategic shift. The company recently unveiled the MacBook Neo, a $599 laptop, powered by the A18 Pro processor, designed to compete directly in the entry-level PC segment, an area historically dominated by Windows laptops and Chromebooks. Early reactions from analysts and industry observers have been strikingly bullish, with Chris Welch at Bloomberg News calling the device a “game-changer” that could expand Apple’s reach to millions of new users and potentially reshape the global notebook market.

The logic behind the optimism is straightforward. By introducing a significantly cheaper MacBook, Apple may unlock a much larger addressable market, particularly among students and first-time buyers. Analysts estimate the device could ship 4 million to 5 million units and help push macOS market share higher even as the broader PC industry faces slowing demand.

If the MacBook Neo succeeds in attracting new users into Apple’s ecosystem, who may later purchase iPhones, services, and other hardware, it could strengthen the company’s long-term growth engine. Considering this aggressive push into the budget laptop market, is Apple stock a buy today?

About Apple Stock

Based in California, Apple stands as a forward-looking company and a worldwide leader in hardware, software, and services. Its portfolio spans iconic devices like the iPhone, iPad, Mac, and Apple Watch, alongside widely used platforms such as the App Store, iCloud, Apple Music, and Apple TV+. The company currently boasts a market cap of $3.8 trillion and a Magnificent Seven status.

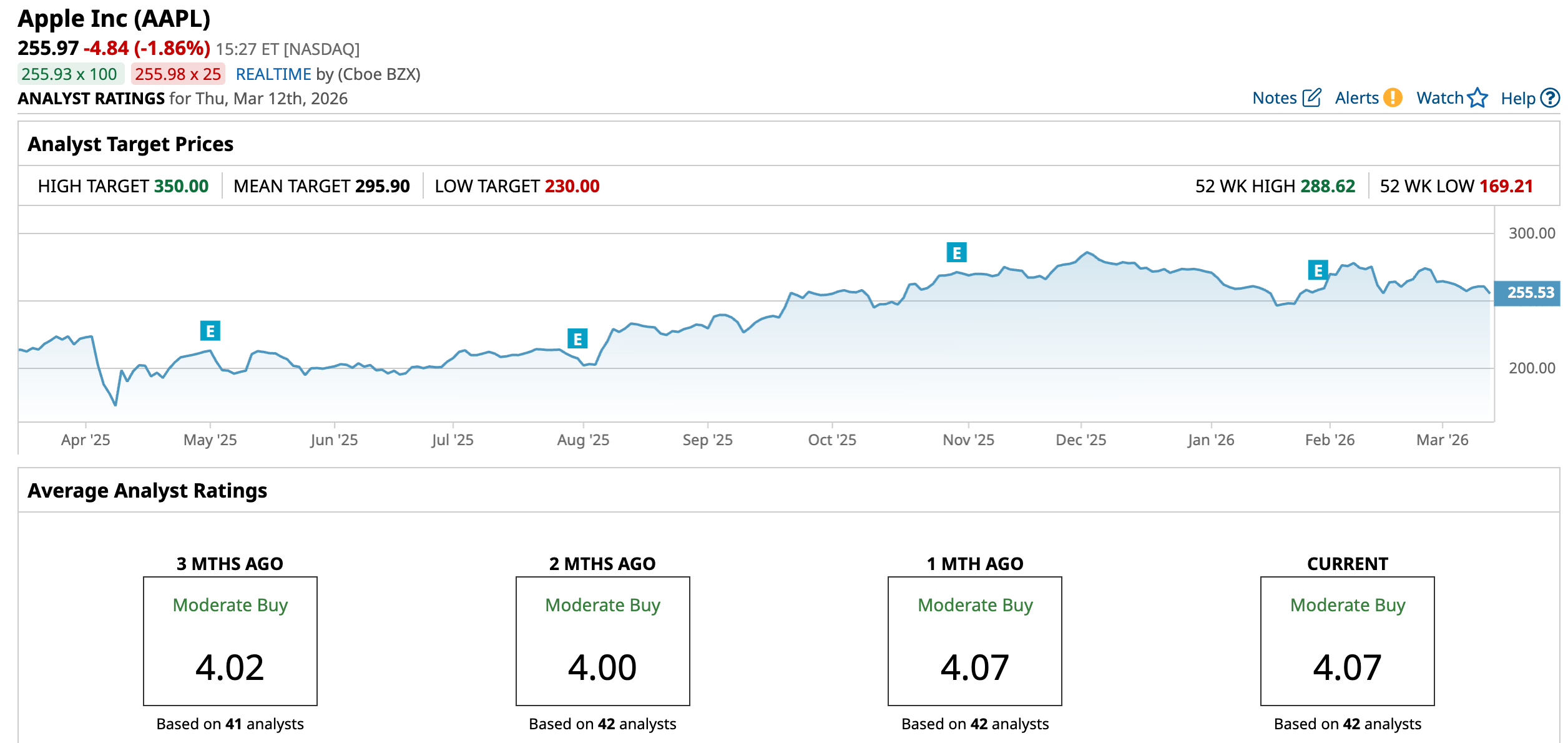

Shares of Apple have delivered stable gains over the past year but have pulled back modestly in 2026. Year-to-date (YTD), Apple shares slumped 6.23%, reflecting some profit-taking after the stock reached record highs in late 2025. The stock is down 11% from its 52-week high of $288.62, reached on Dec. 3. Also, the decline has been influenced by broader volatility across technology stocks and investor caution around global economic conditions and upcoming product cycles.

Despite the recent pullback, Apple is still up by 17.5% over the past 52 weeks, driven by continued strength in the company’s services business, expanding artificial intelligence (AI) capabilities across its ecosystem, and steady demand for premium devices. Notably, the launch of the MacBook Neo did not trigger a major immediate move in Apple’s share price.

The stock is trading at a premium at 31.01 times forward earnings, compared to the sector median and its historical average.

Steady Financial Performance

Apple released its fiscal first-quarter 2026 results on Jan. 29, covering the quarter ended Dec. 27, 2025, and delivered a record-breaking performance driven largely by strong iPhone demand and continued growth in its services ecosystem.

The company reported revenue of $143.8 billion, representing a 16% year-over-year (YOY) increase. Net income climbed to $42.1 billion, up from $36.3 billion a year earlier, while earnings per share rose to $2.84, marking a 19% YOY increase and exceeding Wall Street expectations.

The strong top line growth was primarily driven by the iPhone segment, where revenue surged to $85.3 billion, reflecting a 23.3% YOY jump as global demand for the latest iPhone lineup remained robust. Apple’s services business also delivered record performance, generating $30 billion in revenue, which represented a 14% increase from the prior year, highlighting the continued expansion of high-margin offerings.

Other product categories delivered mixed results. iPad revenue rose to $8.6 billion, improving around 6.3%, while Mac revenue declined about 6.7% YOY to around $8.4 billion, reflecting softer demand in the PC market. The Wearables, Home and Accessories segment generated about $11.5 billion, slightly lower than the $11.7 billion reported in the same quarter last year.

Moreover, management signaled continued momentum in the business. For the March 2026 quarter (fiscal Q2 2026), Apple projected revenue growth of roughly 13% to 16% YOY.

Furthermore, the consensus estimate of $8.41 for fiscal 2026 indicates an increase of 12.7% YOY, before improving by another 10.5% annually to $9.29 in fiscal 2027.

What Do Analysts Expect for Apple Stock?

Earlier this month, Apple received renewed bullish commentary from Evercore ISI, which reiterated its “Outperform” rating and $330 price target after the company refreshed its MacBook lineup. The firm believes the updated MacBook Air and MacBook Pro models improve performance and AI capabilities, while the new MacBook Neo expands Apple’s reach into the midrange PC market.

Moreover, Wedbush reiterated its “Outperform” rating and $350 price target after the company unveiled an updated Mac lineup powered by AI-focused chips.

On the other hand, Rosenblatt slightly raised its price target on Apple to $268 from $267, but maintained a “Neutral” rating.

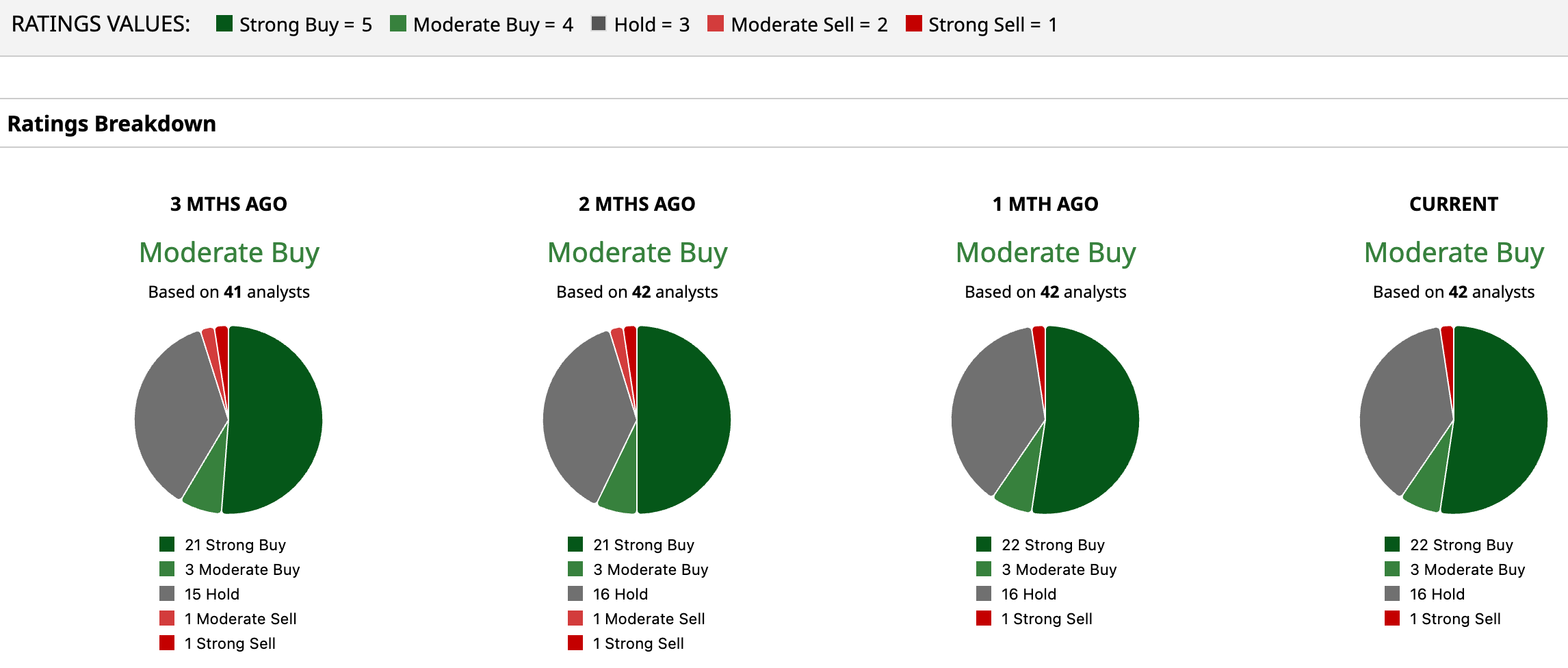

Apple stock has a consensus “Moderate Buy” rating overall. Out of 42 analysts covering the tech giant, 22 recommend a “Strong Buy,” three give a “Moderate Buy,” 16 analysts stay cautious with a “Hold” rating, and one gives a “Strong Sell” rating.

While the average analyst price target of $295.90 suggests an upside of 15.6%, Wedbush’s Street-high target price of $350 suggests as much as 36.7% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart